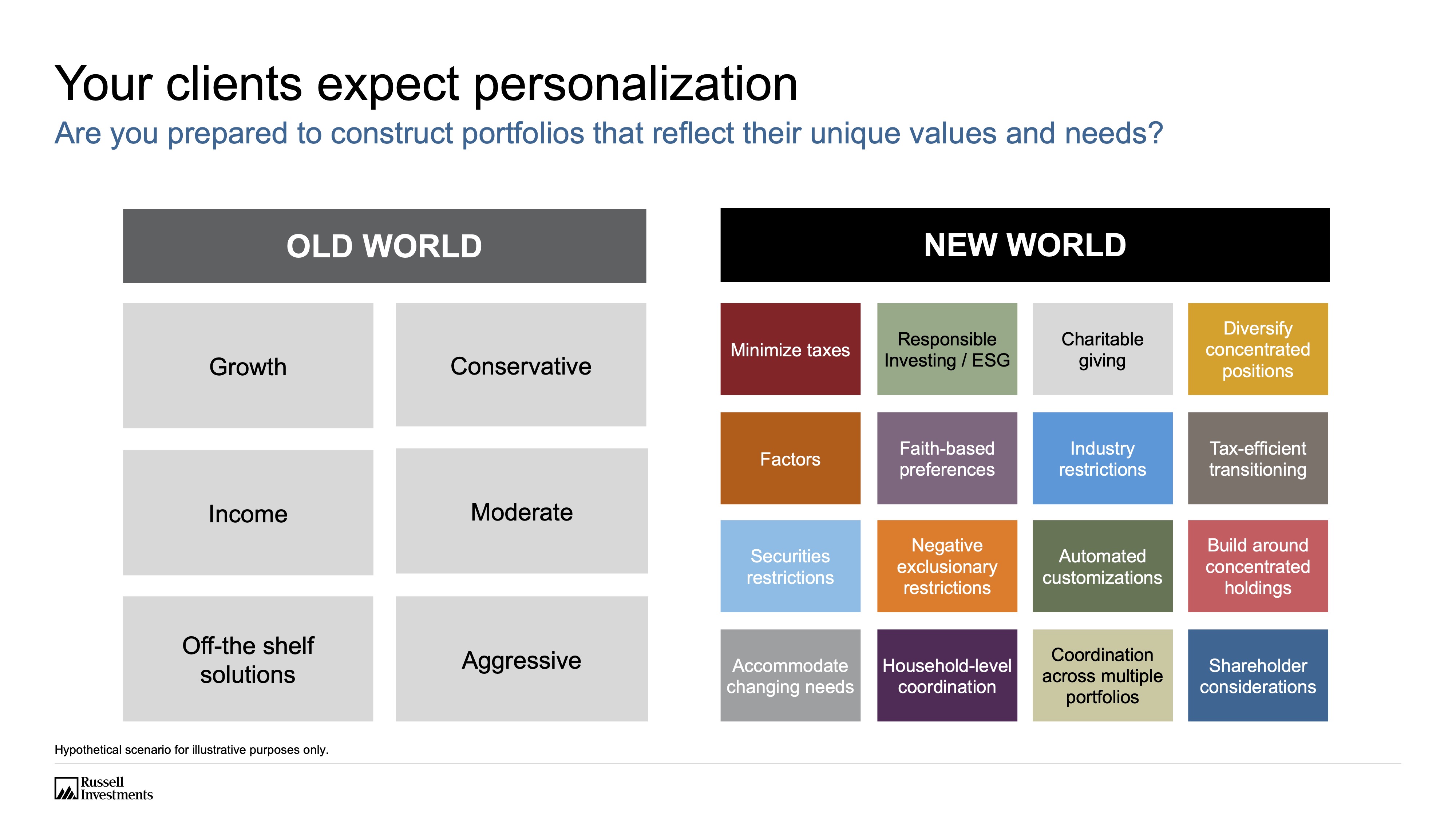

How can investment strategies be tailored to individual needs and goals? A bespoke approach to financial planning offers significant advantages.

Tailored investment strategies are approaches to portfolio management that consider the unique circumstances of each investor. This includes factors like risk tolerance, financial goals (such as retirement, home purchase, or child's education), time horizon, and current financial situation. Instead of a one-size-fits-all approach, these strategies carefully craft a portfolio designed to meet specific objectives. For instance, a young professional aiming for early retirement might favor a more aggressive investment strategy with a higher allocation to equities, while a retiree with fixed income needs might prioritize stability and lower-risk investments. This individualized approach aims to maximize returns while mitigating potential losses based on the investor's unique profile.

The benefits of a customized strategy are substantial. By aligning investments with personal circumstances and goals, individuals can potentially achieve better returns and a higher likelihood of reaching their financial objectives. This personalized approach also fosters greater investor confidence and engagement. Strategies that are relevant and understood lead to better adherence to the plan, increasing the likelihood of success. Furthermore, a bespoke strategy often includes ongoing review and adaptation, ensuring the plan remains effective as life circumstances and market conditions change. This dynamic approach to investment planning promotes financial well-being.

| Individual | Age | Financial Goals | Investment Focus |

|---|---|---|---|

| Jane Doe | 35 | Retirement, Down Payment | Balanced portfolio with moderate risk, stocks and bonds |

| John Smith | 65 | Retirement income | Conservative portfolio with emphasis on fixed income |

The following sections will explore the diverse considerations involved in creating personalized investment strategies, such as risk tolerance assessment, goal-setting methodologies, and portfolio construction principles.

Personalized Investment Strategies

Effective investment strategies require a deep understanding of individual needs and objectives. Tailored approaches optimize portfolio construction, risk management, and the likelihood of achieving financial goals.

- Risk tolerance

- Financial goals

- Time horizon

- Asset allocation

- Market analysis

- Tax implications

- Regular review

- Investment education

These key aspects collectively form a comprehensive strategy. Assessing risk tolerance helps determine appropriate asset allocation. Clear financial goals guide investment choices, aligning with time horizons. Market analysis informs adjustments, while tax implications are crucial for optimal returns. Regular review ensures strategies remain relevant and effective. Investment education empowers informed decision-making. For instance, a retiree aiming for income generation would likely favor a lower-risk portfolio compared to a young investor seeking growth. These individual characteristics drive personalized strategies, increasing the chances of reaching financial objectives.

1. Risk Tolerance

Risk tolerance is a fundamental element in developing personalized investment strategies. Understanding an investor's comfort level with potential losses is critical for crafting a portfolio aligned with their individual circumstances and goals. A strategy that ignores this aspect can lead to significant dissatisfaction or even financial hardship.

- Defining Risk Tolerance:

Risk tolerance represents an individual's capacity to absorb potential financial losses without adverse emotional or behavioral reactions. This isn't merely a mathematical calculation; it considers psychological factors, financial commitments, and time horizons. Someone with substantial savings and a long time horizon before retirement might exhibit higher risk tolerance than someone facing immediate financial needs. Understanding these nuances is crucial for crafting an appropriate investment plan.

- Impact on Asset Allocation:

Risk tolerance directly influences asset allocation. A higher risk tolerance often necessitates a portfolio with a greater proportion of equities (stocks), which historically have demonstrated higher growth potential but also carry greater volatility. Conversely, a lower risk tolerance might dictate a portfolio with a higher allocation to fixed-income securities like bonds, which offer relative stability but typically have lower growth potential. A well-defined risk tolerance profile informs the optimal mix of asset classes to construct a tailored portfolio.

- Influence on Investment Choices:

Risk tolerance significantly impacts specific investment choices. Investors with a high risk tolerance might be more inclined toward emerging market investments or actively managed funds, which often possess higher growth potential. Investors with a lower risk tolerance might prefer more established sectors or low-cost index funds. The choices reflect the investor's willingness to accept fluctuations in market value.

- Importance of Regular Review:

Risk tolerance isn't static; it can evolve over time. Life events, market conditions, or even personal growth can shift an individual's comfort level with investment risk. Therefore, regular review and re-evaluation of risk tolerance is crucial for maintaining a personalized investment strategy that aligns with current circumstances. This proactive approach ensures the portfolio remains suitable and helps avoid potential financial distress.

In summary, integrating a thorough assessment of risk tolerance into personalized investment strategies is essential. This involves understanding how the investor's individual characteristics affect their approach to market fluctuations. By considering factors like time horizon, financial commitments, and potential emotional responses to losses, a portfolio can be constructed that aligns with the investor's overall well-being and long-term financial goals. A dynamically maintained risk tolerance framework further ensures the investment strategy stays relevant and resilient to changing circumstances.

2. Financial Goals

Financial goals are the cornerstone of effective personalized investment strategies. They define the desired outcomes and guide the selection of appropriate investment vehicles and asset allocation. Without clearly defined financial goals, a strategy becomes aimless, lacking a specific target for the investment process. A retirement plan, a down payment on a home, or funding a child's education all serve as distinct goals that necessitate different investment approaches. Understanding the timeframe required for each objective is paramount; a longer horizon permits greater risk-taking than a shorter one.

The significance of financial goals extends beyond simply defining the desired outcome. They influence investment decisions by setting benchmarks for success. For example, a goal of early retirement necessitates a higher allocation to assets with growth potential. Conversely, a goal of maintaining current lifestyle in retirement will prioritize strategies that protect capital while generating steady income. The financial goals should be quantifiable, specifying the desired amount of money for each objective. If the goal is purchasing a home, an amount for a down payment would be critical to understanding the appropriate investment strategy. Without these precise goals, any investment strategy risks being misaligned with the investor's actual needs. This alignment is critical for long-term success. Consider a young professional aiming for a substantial down payment in five years. A portfolio optimized for long-term growth is suitable, with appropriate asset allocation and diversification to mitigate risk. Conversely, an investor nearing retirement with a fixed income need will require a conservative investment strategy to preserve capital.

In essence, financial goals are not merely aspirations; they are critical components of personalized investment strategies. They dictate the investment approach, ensuring the allocation of assets aligns with the investor's specific aims. Understanding the timeframe and the associated financial amounts for each goal is crucial for formulating a sound investment plan, maximizing the probability of achieving desired outcomes. The absence of well-defined financial goals leaves the investment strategy rudderless, impacting long-term financial success.

3. Time Horizon

Time horizon, a crucial aspect of individual circumstances, plays a pivotal role in shaping personalized investment strategies. The timeframe within which an investor intends to achieve financial goals significantly influences appropriate investment choices. A shorter time horizon typically necessitates a more conservative approach, while a longer horizon allows for a more aggressive strategy.

- Impact on Risk Tolerance:

A shorter time horizon often necessitates a lower-risk investment approach. This is because the investor has limited time to recover from potential market downturns. Quick turnaround times for investments are critical in minimizing risk and maximizing the probability of reaching financial targets within the specified timeframe. For example, an individual saving for a down payment on a house in three years will likely avoid high-growth, volatile investments and prioritize assets with lower risk and predictable returns.

- Influence on Asset Allocation:

The time horizon significantly influences asset allocation. A longer time horizon permits a higher allocation to equities, which historically have delivered higher returns but also carry greater risk. Conversely, a shorter time horizon will lean towards more conservative asset classes such as bonds or money market instruments to preserve capital and reduce volatility during the investment period. For instance, a young person planning for retirement in 40 years could comfortably invest more heavily in equities, while someone approaching retirement in five years would likely prioritize capital preservation and stability.

- Strategies for Different Timeframes:

Time horizon profoundly affects investment strategies. Strategies for near-term goals, like a down payment on a home, may focus on high-yield savings accounts, certificates of deposit, or low-risk bonds, while those with a longer time horizon, like retirement planning, might incorporate a larger proportion of stocks and potentially other more complex investments. This nuanced approach ensures alignment between the investment strategy and the investor's specific needs, optimizing the likelihood of meeting financial goals within the given timeframe.

- Dynamic Adaptation:

Time horizons are not static; they evolve with changing life circumstances. A longer time horizon allows for the potential for market fluctuations without drastic consequences. Conversely, a shorter time horizon demands vigilance and careful monitoring. Flexibility and a willingness to adapt the investment strategy based on changing circumstances, market conditions, and the investor's goals are vital. Regular review of the strategy, along with adjustments as needed, ensures that the investments remain aligned with the time horizon and the individual's evolving needs.

Ultimately, recognizing the role of time horizon in personalized investment strategies is essential for developing an effective financial plan. Tailoring strategies to match specific timeframes enhances the likelihood of achieving desired financial outcomes and promotes investor confidence. Flexibility and adaptation are key to maintaining alignment between the investment strategy and the evolving time horizon and goals of the individual investor.

4. Asset Allocation

Asset allocation is a cornerstone of personalized investment strategies. It involves the strategic distribution of investments across various asset classeslike stocks, bonds, real estate, and cashto align with individual investor objectives. Proper allocation reflects an investor's risk tolerance, financial goals, and time horizon, thereby maximizing the potential for achieving desired outcomes while mitigating potential risks. A well-defined asset allocation plan provides a framework for a robust and personalized investment strategy.

- Risk Tolerance Considerations:

Asset allocation directly responds to risk tolerance. Investors with a high tolerance for risk might favor a portfolio with a larger allocation to stocks, anticipating potentially higher returns but accepting greater volatility. Conversely, lower risk tolerance often leads to a portfolio tilted towards safer assets like bonds or cash. This tailored approach reflects individual comfort levels with market fluctuations. For example, an investor nearing retirement might prefer a portfolio with a lower stock allocation to protect accumulated capital, while a younger investor with a longer time horizon might feel comfortable with a higher percentage of stocks. The proper allocation is therefore highly individualized.

- Financial Goal Alignment:

Asset allocation aligns with financial objectives. A portfolio aimed at retirement often features a higher proportion of stocks for potential growth in the earlier years, transitioning to a more conservative asset allocation as retirement nears. Conversely, a portfolio supporting a down payment might have a shorter time frame and will require a different balance of assets. This dynamic adjustment ensures the investment strategy supports the evolving goals of the investor. A diversified allocation ensures a strategy that supports varied financial milestones over the investor's life cycle.

- Time Horizon Impact:

Time horizon dictates the appropriate asset allocation. A longer time horizon permits greater exposure to higher-growth assets like stocks, allowing potential gains to compound over a longer period. Conversely, a shorter horizon might demand a more conservative allocation to assets that provide stability and capital preservation. The investment approach adapts to the longevity of the investment period. The longer the time frame, the more flexible the asset allocation can be. The shorter the time frame, the greater the need for caution and capital preservation.

- Diversification Benefits:

Asset allocation fosters diversification. Distributing investments across various asset classes reduces the overall portfolio risk. If one asset class underperforms, others may compensate. This mitigates the impact of market fluctuations and helps maintain portfolio stability. This approach reflects a balanced strategy, recognizing that different asset classes behave differently in the market.

In conclusion, asset allocation is an integral component of personalized investment strategies. It serves as a framework that accounts for risk tolerance, financial goals, and time horizon. By strategically distributing investments across diverse asset classes, investors can achieve better risk-adjusted returns and maximize the potential for reaching financial objectives. A well-defined allocation is essential for successful long-term investment planning, reflecting the diverse needs and aspirations of each individual investor.

5. Market Analysis

Market analysis is an indispensable element of personalized investment strategies. Understanding market trends and potential fluctuations is crucial for adapting investment portfolios and maximizing the likelihood of achieving financial goals. Accurate analysis helps inform choices, guiding adjustments to asset allocation and risk management, and providing a crucial framework for strategy refinement. This allows investors to remain responsive to evolving market conditions and to optimize their investment portfolios over time. Effective market analysis helps anticipate potential risks and opportunities.

- Identifying Market Trends:

Recognizing underlying market trends is paramount. Analyzing economic indicators, such as interest rates, inflation, and unemployment, provides crucial context for investment decisions. Monitoring industry-specific trends and technological advancements offers insights into sector-specific performance and potential for growth. These insights enable a nuanced understanding of market direction, facilitating strategic adaptation of personalized investment strategies.

- Evaluating Market Volatility:

Evaluating market volatility is essential. Analyzing historical data and identifying patterns of market fluctuations helps investors assess potential risks and opportunities. This crucial insight informs risk mitigation strategies and the appropriate allocation of assets. By understanding historical volatility patterns, investors can adapt their personalized investment plans to respond proactively to market shifts.

- Assessing Sector Performance:

Examining sector-specific performance provides valuable insights. Analyzing the growth and decline of different industry segments allows informed decisions regarding sector allocation within a portfolio. This granular analysis helps maintain a balance among diverse investment options, ensuring the portfolio stays aligned with broader market trends. Understanding which sectors are likely to flourish and which may face challenges enables informed adjustments to a personalized investment strategy.

- Forecasting Potential Impacts:

Anticipating potential impacts on investment returns is critical. Thorough market analysis enables forecasting potential outcomes based on current trends and potential future events. This forward-looking approach allows investors to modify their strategy in response to emerging market conditions, adjusting the portfolio accordingly. Using such foresight, personalized investment strategies can be proactive in adjusting to evolving market conditions and improving long-term performance.

Incorporating market analysis into personalized investment strategies enhances the ability to adapt to shifting market conditions. By considering trends, volatility, sector performance, and potential future impacts, investors can make well-informed decisions. This proactive approach not only mitigates risks but also capitalizes on emerging opportunities, ultimately increasing the likelihood of achieving desired financial outcomes. A dynamic and responsive approach to market analysis is paramount for the successful implementation of personalized investment strategies.

6. Tax Implications

Tax implications are integral to effective personalized investment strategies. Understanding how various investment choices interact with tax codes is crucial for optimizing returns and minimizing liabilities. Tax laws vary significantly, necessitating tailored strategies to accommodate individual circumstances and maximize post-tax returns. Ignoring these complexities can lead to unforeseen tax burdens, potentially impacting overall financial well-being. A strategic approach to taxes is essential for the success of any well-defined investment plan.

- Capital Gains and Losses:

Capital gains and losses represent a significant tax consideration. Different asset classes, such as stocks, bonds, and real estate, have varying tax treatment. Recognizing these differences is essential for minimizing tax burdens. For instance, short-term capital gains are typically taxed at higher rates compared to long-term gains. Understanding these distinctions empowers investors to optimize strategies for capital appreciation and effectively manage capital gains tax liabilities.

- Dividend Income:

Dividend income from investments also carries tax implications. Different types of dividends, such as qualified and non-qualified dividends, are taxed at different rates. Accurate classification and appropriate tax planning can significantly impact the overall return on investments. Investors need to account for dividend income in their calculations to accurately understand total investment returns after taxes.

- Tax-Advantaged Accounts:

Utilizing tax-advantaged accounts, such as 401(k)s and IRAs, can significantly reduce tax burdens. These accounts allow contributions to grow tax-deferred, potentially leading to substantial savings at retirement. However, understanding the specific rules and limitations of these accounts is critical, as withdrawal strategies in retirement also carry tax consequences. Strategies for investment within these accounts must carefully consider these long-term implications.

- Deductions and Credits:

Certain investment-related expenses and activities may qualify for deductions or credits. Understanding available deductions and credits can significantly reduce the overall tax burden. For example, investment advisory fees or eligible educational expenses associated with investment knowledge enhancement may be deductible in certain circumstances. Consulting with a tax professional ensures investors maximize these potential savings.

In conclusion, incorporating tax implications into personalized investment strategies is not simply a compliance matter but a vital component of financial optimization. By understanding and proactively addressing tax considerations, investors can potentially maximize their returns after taxes and ensure their investment strategies align with their broader financial goals. Navigating the complexities of tax laws is an important responsibility for all investors aiming for long-term financial security.

7. Regular Review

Regular review is an indispensable element of effective personalized investment strategies. Consistent evaluation of investment performance, market conditions, and evolving financial circumstances ensures strategies remain aligned with objectives. This proactive approach allows adjustments to be made before significant deviations occur, safeguarding against misalignment and potential losses.

- Adapting to Changing Circumstances:

Life events, such as marriage, childbirth, career changes, or health issues, can significantly impact financial goals and risk tolerance. Regular review allows strategies to be adjusted accordingly. For instance, a significant inheritance might warrant a revised asset allocation, while a sudden increase in living expenses might necessitate a temporary reduction in risk exposure. This adaptability ensures the investment plan remains relevant and responsive to life's transitions.

- Monitoring Market Fluctuations:

Market conditions are dynamic. Regular review enables swift adjustments to changing market environments. For example, if a sector experiences a downturn, the portfolio can be rebalanced to reduce exposure to that sector. Conversely, if a sector demonstrates promising growth, the portfolio can be adjusted to capitalize on potential gains. This responsiveness to market shifts is vital for mitigating risk and optimizing returns.

- Assessing Portfolio Performance:

Regular review allows evaluation of actual investment performance against projected targets. This comparison highlights discrepancies between expected results and realized outcomes. If performance deviates significantly, adjustments can be made to correct course. This systematic evaluation helps ensure the strategy remains on track and effectively serves the investor's long-term objectives. For instance, if a portfolio underperforms its benchmark, strategies can be updated to address the underperformance.

- Maintaining Alignment with Goals:

Reviewing the investment strategy against ongoing goals helps maintain alignment. Goals may change, and the investment strategy must evolve accordingly. Regular reviews allow for this adaptation. For example, a retiree's need for steady income necessitates a shift in asset allocation towards more income-generating investments as retirement approaches. Regular review ensures the strategy continues to support evolving financial goals.

In conclusion, regular review is not a one-time event; it is a continuous process. By integrating regular assessments of market conditions, financial circumstances, and investment performance, personalized investment strategies can be adjusted to maintain alignment with goals, adapt to changes, and maximize the likelihood of achieving desired outcomes. This proactive approach significantly enhances the long-term success of any investment plan, facilitating the achievement of long-term financial security.

8. Investment Education

Investment education is fundamental to the development and execution of effective personalized investment strategies. A well-informed investor possesses the knowledge and skills necessary to navigate the complexities of the financial markets, making sound choices aligned with individual circumstances and goals. Without this knowledge, investors may rely on flawed strategies or inadequate information, potentially leading to suboptimal outcomes.

- Understanding Financial Concepts:

Investment education equips individuals with a comprehension of fundamental financial concepts, including risk tolerance, asset allocation, diversification, and return expectations. This knowledge empowers informed decision-making, enabling individuals to select suitable investment instruments and strategies. Knowledge of compound interest, for example, is crucial for long-term investment success, motivating individuals to make strategic choices for future financial gain.

- Developing Critical Thinking Skills:

Investment education fosters critical thinking skills essential for evaluating investment opportunities and identifying potential risks. Learning to assess financial information objectively, discern misleading information, and evaluate market trends are crucial skills. This critical evaluation is vital for developing an investment strategy aligned with personal circumstances.

- Recognizing Personal Financial Goals:

Investment education helps individuals clearly define their financial goals, such as retirement planning, home purchases, or education funding. This clarity aids in matching investment strategies to specific goals. Understanding the timeframe for achieving goals provides a crucial context for investment decisions, helping individuals make informed choices, such as whether to prioritize growth or stability.

- Adapting to Changing Markets:

Investment education equips investors with the tools to understand market fluctuations and adapt investment strategies. Recognizing potential risks and opportunities allows investors to make adjustments to their portfolios to maximize returns and minimize losses. Staying informed about market dynamics, such as inflation or economic cycles, empowers individuals to dynamically adjust their strategies over time.

In essence, investment education serves as the bedrock for personalized investment strategies. A well-educated investor is better positioned to craft a strategy that aligns with individual circumstances and objectives, making sound financial decisions that support long-term financial well-being. This knowledge empowers individuals to actively participate in building their financial future. Comprehensive investment education fosters a greater understanding of risk tolerance, return expectations, and suitable investment options.

Frequently Asked Questions about Personalized Investment Strategies

This section addresses common inquiries regarding personalized investment strategies, providing clear and concise answers to help investors navigate the complexities of tailored financial planning.

Question 1: What distinguishes a personalized investment strategy from a generic one?

A generic investment strategy employs a one-size-fits-all approach, typically neglecting individual factors such as risk tolerance, financial goals, and time horizon. A personalized strategy meticulously considers these unique characteristics, creating a portfolio tailored to the specific needs and circumstances of the investor. This targeted approach aims to optimize returns while managing risk in accordance with the investor's unique profile.

Question 2: How is risk tolerance assessed in a personalized investment strategy?

Risk tolerance assessment involves a multifaceted evaluation. Factors such as an investor's financial situation, investment experience, and emotional response to market fluctuations are considered. Professional advisors often employ questionnaires and discussions to comprehensively gauge an investor's comfort level with potential losses and market volatility. This assessment is pivotal in shaping the optimal asset allocation for the portfolio.

Question 3: Can personalized investment strategies adapt to changing life circumstances?

Absolutely. Life events like marriage, career transitions, or the birth of children often alter financial goals and risk tolerance. A personalized investment strategy, by its nature, is flexible and adaptable. Regular reviews and adjustments to asset allocation ensure the strategy remains aligned with evolving circumstances, maintaining alignment with long-term financial objectives.

Question 4: What role does time horizon play in a personalized strategy?

The time frame within which an investor aims to achieve financial goals significantly influences asset allocation. A longer time horizon permits a more aggressive investment approach, potentially embracing higher-growth assets. Conversely, a shorter time horizon necessitates a more conservative strategy, emphasizing capital preservation. The strategy's dynamic adjustments reflect the anticipated timeframe for achieving the defined financial objectives.

Question 5: Are there specific costs associated with personalized investment strategies?

Costs vary depending on the service provider and the scope of the strategy. Fees may be associated with advisory services, investment management, or portfolio maintenance. It's essential to inquire about and compare fees from different providers to ensure they align with the investor's budget and expected returns. Transparency in fees and associated charges is crucial.

Understanding these common questions empowers investors to make informed decisions about personalized investment strategies, leading to a more well-defined and effective financial plan.

The subsequent sections will delve deeper into the practical applications of personalized strategies, offering insights into different investment vehicles and the importance of consistent portfolio reviews.

Conclusion

Personalized investment strategies represent a crucial shift in financial planning. Moving beyond generic approaches, these strategies meticulously consider individual investor circumstances, including risk tolerance, financial objectives, and time horizons. Key elements, such as asset allocation, market analysis, and tax implications, are tailored to optimize returns while mitigating risks. Regular review and adaptation are paramount to maintain alignment with evolving needs and market conditions. The tailored nature of these strategies fosters a higher likelihood of achieving long-term financial goals by accounting for unique investor profiles. A comprehensive understanding of these elements is essential for responsible and effective wealth management.

The increasing complexity and volatility of financial markets underscore the critical importance of personalized strategies. While generic approaches may offer a degree of simplicity, they often fail to address the nuances of individual needs. Moving forward, the adoption of personalized investment strategies will likely become more prevalent as investors seek to maximize returns and minimize risk within the context of their unique financial journeys. A proactive approach to financial planning, informed by personalized strategies, remains essential for securing long-term financial well-being.

You Might Also Like

Jimmy Hawkins Net Worth 2024: A Deep DiveVanguard VTSAX Vs VTSIX: Which ETF Is Right For You?

2000 Krona To USD: Current Exchange Rate & Converter

Firefighter Drug Tests: Policy & Procedures

Mike Vick's Fox Sports Salary: Latest Earnings Revealed

Article Recommendations

- Boomer Esiason Nfl Legend Beyond

- Luke Roberts Family Insights Discover Their Life And Legacy

- The Enchanting Journey Of Georgie Henley Movies And Tv Shows